By Steven Neeley, CFP®

According to a recent article in Financial Advisor Magazine, total U.S. annuity sales increased by 22% this year to $77.5 billion, eclipsing the previous record set during the financial crisis in 2008. Nothing sells like fear!

Interest rates have soared since the beginning of the year, with the 10 Year Treasury yield rising from 1.7% at the beginning of 2022 to nearly 3.3% presently. Have they risen enough to make annuities an attractive investment?

In full disclosure, I’ve never recommended that a client buy an annuity, though I’ve explored immediate annuities for clients on multiple occasions. The main problem I’ve always run into is that the rate of return on annuities has been so low that it made no sense for clients to lock up their money when there were other viable options.

Many fee-only advisors take a dim view of annuities and those who sell them, but I’m not sure that’s fair, and let’s be honest, if you are truly a fiduciary, you have an obligation to find the best solution for your clients regardless of your opinion of certain products. So, let’s find out if annuities are attractive at the moment.

Annuity Types?

There are a wide variety of annuities out there: immediate, deferred, variable, indexed, and so on. The focus of this article is on single premium immediate fixed annuities (SPIA) for a few reasons:

- Comparing the various options goes well beyond the scope of this article.

- You can make a case for an SPIA as part of a retiree’s well-diversified portfolio, especially one who is highly risk averse and wants the surety of knowing their income needs are going to be met regardless of what is happening in the financial markets.

- The other annuity options tend to be expensive and difficult to understand. What’s more, I’ve always found that the problems they claim to solve can often be solved in other, often simpler, ways. For example, if you like the fact that there is upside potential with a guaranteed floor on an indexed annuity, you could create a very similar payoff simply by holding more cash than stocks.

Analysis

I used the website AnnuityFYI.com to get quotes from multiple carriers. I compared two scenarios:

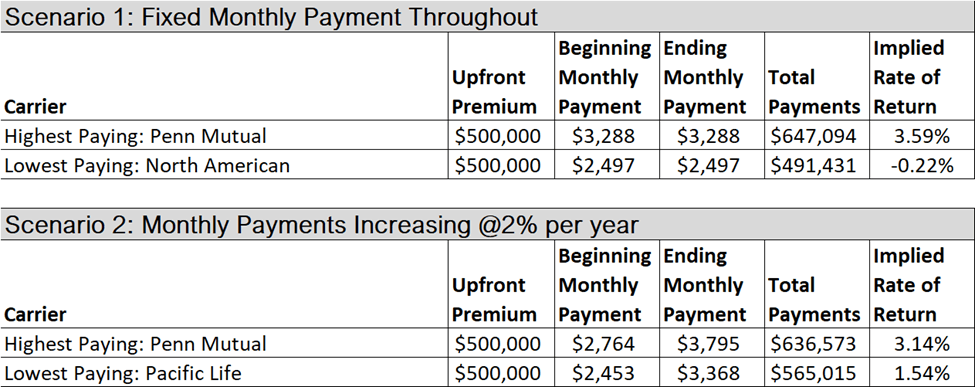

Scenario 1

- Fixed monthly payments through the life of the contract

- Single premium – $500,000

- 68-year-old male

Scenario 2

- Monthly payments that are increased by 2% annually to protect from inflation

- Single premium – $500,000

- 68-year-old male

In both scenarios, I assumed that the life expectancy was 16.4 years, or roughly 85 years of age, which I got from the Social Security online life expectancy calculator. From this, I backed into the implied rate of return using Microsoft Excel’s IRR function.

Results

The highest implied return came out to about 3.6% a year while the lowest-paying option actually had a negative return. If you chose the North American policy and only lived for 16.4 years, the total payments would be less than the $500,000 paid in. Ouch.

What might be most surprising is that the rates of return for the inflation-adjusted policies were lower than the regular fixed policies. It would take almost 19 years before the cumulative payments from the inflation-adjusted Penn Mutual policy surpassed the equivalent fixed payment policy.

Verdict

The implied rates of return on immediate annuities are still way too low to make them attractive investments. A big part of the problem is that insurance companies still aren’t able to invest at attractive long-term rates, which limits their ability to offer higher returns to annuity purchasers. Sure, cash actually pays something now unlike most of the last decade, but the problem for insurers is that 20 Year Treasury Bonds only yield about 3.6% at the moment, right in line with the implied return on the fixed payment Penn Mutual annuity. If you consider that inflation is running at 9% right now, a 3.6% rate of return isn’t very appealing.

Of course, everyone’s situation is different and as I noted above, annuities can make sense given the right set of circumstances. That said, for most people, there is no reason to rush out and buy one right now. Better to maintain flexibility and wait for a more attractive opportunity.

Steven Neeley, CFP® is an investment advisor representative of and offers investment advisory services through Fortress Capital Advisors LLC, a registered investment advisor offering advisory services in the State of Indiana and other jurisdictions where registered or exempted. Main office: 4841 Industrial Pkwy, #139, Indianapolis, IN, 46226. Tel: (317) 210-3727.