Are you prepared for retirement?

Preparing for retirement can be overwhelming, but don’t worry because we’re here to help!

With some professional guidance and a checklist of steps to take to make sure you are prepared for retirement, you can be successful even if you are late to the game.

In this paper, we outline the most critical steps you must take to ensure that you are prepared for retirement.

Prioritize Which Accounts You Will Save In

I. Get the employer match – If your employer offers a match on retirement account contributions, you should almost always take advantage of it. If you don’t, you are literally leaving money on the table.

II. Health Savings Account – There are so many advantages to using health savings accounts

a. Contributions are not only tax deductible, but you also avoid paying FICA taxes on them.

b. You can own stocks, bonds, and mutual funds in an H.S.A. account just like you can in a regular brokerage account.

c. The account grows tax-free and withdrawals are also tax-free as long as they are used for qualified medical expenses.

A 2022 study by Fidelity Investments found that couples 65 and older can expect to spend close to $315,000 after-tax dollars on health and medical expenses throughout retirement. Spending that kind of money on health care could wreck your retirement plans, which is why we rank H.S.A.s so high.

III. Max out retirement plans – This could be either pre-tax retirement plans like traditional 401(k)s and IRAs or after-tax retirement plans such as Roth 401(k)s and Roth IRAs.

A lot of financial gurus pound the table about saving in Roth accounts, but the case for doing so isn’t cut and dry. Depending on your current and your expected tax situation after retirement, you might be better off saving in a traditional, pre-tax retirement account.

We suggest having a professional run a scenario analysis to determine which option makes the most sense for your specific situation.

IV. Saving in a taxable brokerage account – While we have this last, it’s still a critical piece of the retirement planning puzzle.

Taxable brokerage accounts offer the most flexibility with regard to the types of investments you can own in them. Also beneficial is the fact that there are no withdrawal penalties on these accounts.

Ultimately, having a mix of tax-free, tax-deferred and taxable investment accounts allows you to maximize tax efficiency by strategically placing different investment types in the account that allows you to minimize taxes.

Create a Withdrawal Strategy

Just as it’s important to know which accounts to prioritize for savings, it’s also important to have a well-thought-out strategy for prioritizing which accounts to withdraw from.

Whether your ultimate goal is donating your estate to charity, bequeathing it to heirs, or a combination of both, nearly everyone wants to make sure that their savings lasts throughout their lifetime.

To accomplish this, not only do you need to come up with a plan regarding when to start withdrawing from your investment accounts, but you also need to figure out the order in which you will withdraw from your accounts.

For example, if you have a Roth IRA, a traditional IRA, a taxable brokerage account and a savings account, you need to put some thought into which accounts you should start spending down in order to pay less in taxes and ultimately make your money last as long as possible.

Optimize Investment Placement for Tax Efficiency

To the extent possible, you need to make sure that you place investments in the account that minimizes the amount of taxes you need to pay. All else equal, the less you pay in taxes, the longer your money is going to last.

As a rule of thumb, it’s common to put taxable bonds in tax-deferred accounts like IRAs while putting tax-free municipal bonds in taxable brokerage accounts. It’s also usually more favorable to put stocks in taxable brokerage accounts given that capital gains taxes tend to be much lower than the ordinary income taxes that investors pay on interest income.

Update Your Retirement Plan

- How much you can spend vs. how much you have budgeted.

- How long you can expect your money to last.

- A scenario analysis for determining your needs and the best course of action.

- A lump sum vs annuity pension analysis (if applicable).

Run a Social Security Analysis

Conventional wisdom holds that you should always wait to take Social Security until you have maximized the benefits. And this makes sense for a lot of people, but it may not always be the best option.

Your current health and medical history, financial situation, and ultimate goals all need to be considered before deciding when to take Social Security.

Pay Off Your Debts

Like everything, there are always exceptions to the rule. Nevertheless, it’s generally best to have all your debts paid off, including your mortgage, before retirement.

The psychological benefit of knowing that no matter what happens, you don’t owe anyone anything is liberating and reason enough to do this.

Build a Cash Reserve

We advise our clients to keep one year of expected withdrawals on hand in the safest and most easily accessible form possible. Then every month we distribute 1/12 of the next year’s spending from the client’s brokerage account to top the cash reserve off, always maintaining a steady balance.

Yes, having a year’s worth of cash on hand might be suboptimal if you only care about return on investment. But humans aren’t robots and the peace of mind that comes from knowing that all of your expenses for the year are covered regardless of what happens in the financial markets is priceless.

Remember, retirement should be about enjoying your life, not maximizing return on investment!

Review Your Estate Plan and Beneficiaries

Think Through How You Would Like to Spend Your Retirement

Leaving a career behind can be a lot more difficult than you think, particularly for those who derived a great deal of satisfaction from their jobs.

Often times they find that retirement is not what they thought it would be, leaving them feeling lost and depressed.

The happiest retirees usually find a new purpose in retirement. Common activities include:

Leaving a career behind can be a lot more difficult than you think, particularly for those who derived a great deal of satisfaction from their jobs.

Often times they find that retirement is not what they thought it would be, leaving them feeling lost and depressed.

The happiest retirees usually find a new purpose in retirement. Common activities include:

- Volunteering

- Socializing and finding new friends

- Staying in shape

- Learning new things

- And travel

Make Sure Your Portfolio Allocation Is Appropriate

This is a big one and unfortunately, a lot of people get it wrong. We can’t tell you how many times we’ve reviewed a prospective client’s portfolio that was invested way too aggressively right before the client wanted to retire and start taking withdrawals.

To be sure, it’s a tough balancing act. On the one hand, you need to make sure that your portfolio earns enough to get you safely through retirement, meaning you can’t be too conservative.

On the other hand, being too aggressive can have disastrous consequences, especially if you hit a string of bad returns right when you retire and start withdrawing from your portfolio to live.

This is what is referred to as ‘sequence risk’, which relates to the order of returns, not just the total return.

For example, if you experienced 3 years of negative returns over a 10-year period, whether those returns happened at the beginning or end of the 10-year period makes a big difference if you are withdrawing from your portfolio over that time span.

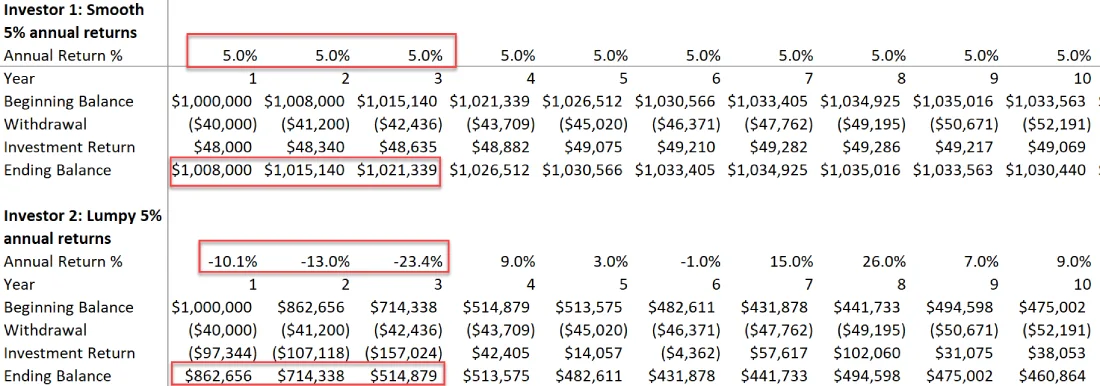

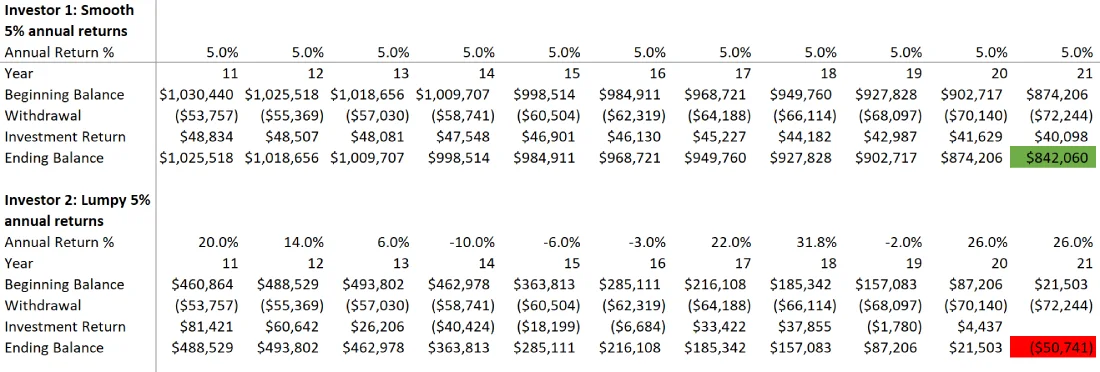

Here’s an illustration to demonstrate the point:

We have two investors who both start with $1,000,000 portfolios. Both withdraw $40,000 per year increasing by 3% annually to account for inflation. And both portfolios compound annually at 5% per year after taxes, fees, etc.

The difference is that Investor 1 earns a steady 5% every year on his portfolio with no variance while Investor 2 has far lumpier returns, ranging between -23% and +32% in a given year. Also notice that Investor 2 earns negative returns for the first 3 years.

Despite both portfolios compounding at 5% per year, the difference in values is striking. Unfortunately for Investor 2, the disastrous performance over the first three years means she will never catch up. By the end of year 10, her portfolio is worth less than half that of Investor 1’s.

Same exact return, but two different return sequences and drastically different outcomes. So how do you prevent yourself from experiencing Investor 2’s fate? Well, there are a couple of ways.

First, you could spend less. If that’s your plan, however, I’m afraid you’ll find it’s not very realistic.

We believe the best approach is to make sure that your portfolio is dialed in before retirement. And that means a couple of things:

a.) You should have a well-thought-out risk management plan in place for when to be defensive, but also for when to be fully invested.

b.) You should put a lot of effort into portfolio construction so that you are combining investments that complement one another and behave differently during a crisis.

A lot of historically uninformed investors got burned in 2022 because they thought that bonds were a safe investment that would gain in value when stocks declined. They learned the hard way that this isn’t always the case.

We often advise clients to replace much of their bond portfolio with investment strategies that work differently than stocks and bonds such as market-neutral and trend-following strategies.

Those types of strategies are far less sensitive to interest rate movements than bonds, i.e., they provide a true diversification benefit, and they also tend to do quite well when stocks sell off.

Other Considerations

a.) Consider hiring professional help According to a study published by the market research firm Morningstar:

“Overall, we estimate that the ‘average’ investor is likely to benefit significantly from working with a financial advisor, even if the services are entirely related to building and monitoring the portfolio… Providing other financial planning services (i.e. financial planning gamma), such as savings guidance, pension optimization, insurance planning, withdrawal planning, etc. are likely to result in even more value for the client…”

Even if you don’t want to hire an advisor to manage your investments, you can hire a financial planner on an hourly basis to help in all the areas mentioned in this paper.

Hiring a financial planner to help with this process should lead to better outcomes while providing you with peace of mind from knowing that you are going down the right path.

b.) DO NOT REACH FOR YIELD! – You may have noticed that there is nothing in this paper about building an income portfolio that will meet your spending needs. That’s because this is a dangerous strategy that can lead to very poor outcomes.

In a world in which government bonds pay low interest rates, it’s tempting to “stretch for yield” by investing in high-income producing assets like closed-end funds, master limited partnerships, business development companies, real estate investment trusts, and junk-rated corporate bonds.

Don’t fall for the temptation! There’s a reason these investments pay high dividends/interest rates. It’s because they are risky.

Moreover, these high-yielding investments are often highly correlated to the economy and do very poorly during recessions. During the Covid scare and during the 2008/2009 financial crisis, high-yielding portfolios typically lost 35% to 50% of their value.

Given how dangerous sequence risk is for retirees, allowing for the possibility of taking on such large losses, even if you eventually recover, simply isn’t worth it.

Conclusion

In conclusion, preparing for retirement is a comprehensive task that requires meticulous planning, careful decision making, and a systematic approach to managing finances. This paper has outlined ten critical steps to help you navigate the complex landscape of retirement planning. The steps range from prioritizing savings accounts and creating a withdrawal strategy to optimizing investment placements for tax efficiency, building a cash reserve, and reviewing your estate plan and beneficiaries.

Retirement should be a time of peace, fulfillment, and financial stability, and with careful preparation and foresight, it can be. Remember, the journey to a successful retirement is not about maximizing return on investment; it’s about ensuring that you are financially secure to enjoy your life.