Market Update: December 2023

“So now that I’ve bashed someone else’s bad investment call, allow me to make a fool of myself by making my own: I expect a strong finish to the year.

September, the historically worst month, is out of the way. Would I be surprised to see September’s sell off extended into October? No.

Having said that, November and December are traditionally pretty good months. More importantly, years that begin as strongly as 2023 tend to have strong finishes.

So, there you have it. Feel free to make fun of me in January if the markets have crashed and we’re in the middle of a massive recession.

Right now, none of the market crash indicators with any sort of predictive power are flashing red. When that changes, we will be prepared to take defensive measures. In the meantime, ignore the investment gurus on CNBC.”

Nailed it!

I kid. I kid. I can’t really thump my chest. If we were married,this is when you would categorically call up every time I’ve made a wrong prediction and throw it in my face. I’ll make it easy for you and just admit that you could find plenty of examples.

Still, I’m now tempted to continuously call for a market correction until we get one.They happen about every 1.5 years, so we shouldn’t have to wait too long.

Then I can run two ‘Advisor Who Called X…’ ads that will never be wrong: a bullish ad featuring my correct call on the rally, and a bearish ad on my stock market correction call. Seems there’s a lot of that going on out there.

Anyway, we had a very nice Santa Claus rally to end the year and for that, we can be grateful. Nearly every asset class rose in tandem to end the year, erasing much of 2022’s losses.

How Did We Get Here?

What led to 2023’s market gains? I could provide a lengthy list, but this year’s returns largely boil down to two things:

1. Stocks love to climb a wall of worry

It is very unsatisfying to admit that much of investing can be boiled down to nothing more than the difference between expectations versus reality. It’s nevertheless true.

Expectations for both stocks and bonds were quite low coming into 2023, yet company earnings largely exceeded expectations while inflation conditions came down more than expected, bolstering bond prices.

2.The Federal Reserve Bank

Have I mentioned how sick I am of talking about the Fed? Oh, right. Yes, many times.

But of course, we can’t avoid talking about it. To the extent that “hawkish” statements made by Federal Reserve Chairman Jerome Powell in August can be blamed on September/October’s sell off, we must give him credit for “dovish” comments in November that helped boost stock and bond prices through yearend.

In short, the market finished the year strong on the expectation that the Federal Reserve will start lowering interest rates next year.

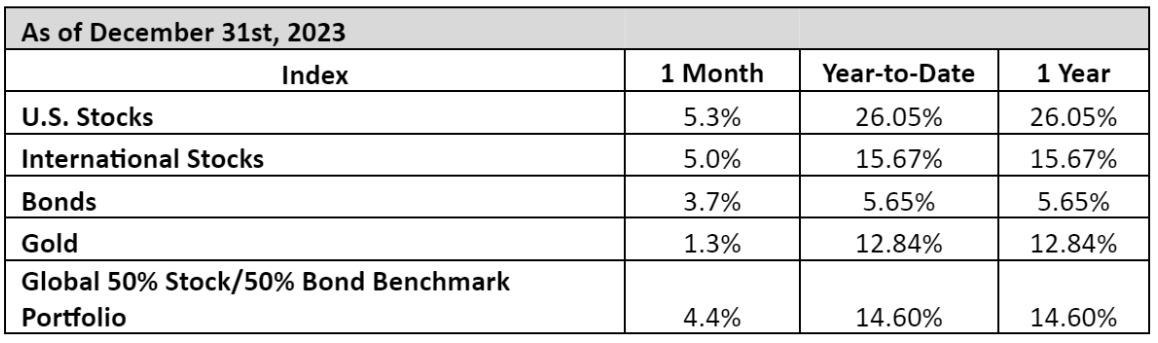

Global Indices

- Once again, U.S. stocks continued their dominance over international stocks. A large part of the underperformance of international stocks was due to the poor performance of Chinese stocks, which continue to suffer from the bursting of the property bubble, as well as the erratic policies put forth by the Chinese Communist Party.

- Bonds staged quite a comeback over the last 3 months of the year. They entered the final quarter down about 1% on a total return basis but ended up more than 5% by year-end.

- Gold also had a nice run at the end of the year. Essentially, bonds became less attractive after interest rates dropped, pushing more investors to gold.

Moving forward

And now for the fun part: thinking about the year ahead.

There are so many things that could go wrong, it’s hard to know where to begin. Let’s try, though.

- Another wild election

- Escalation of the conflict in the Middle East

- A war between China and Taiwan

- Another pandemic

- Inflation perking back up and forcing the Fed to raise interest rates

- NATO getting dragged into the Ukraine war.

I could go on, but you get the point. It’s a scary world out there. Just imagine all the scary things we haven’t even considered. After all, I don’t remember anyone predicting the Ukraine and Israel wars, or the pandemic for that matter.

But before you go doomsday prepper on me, let’s talk about why things, at least for the markets, could be good next year.

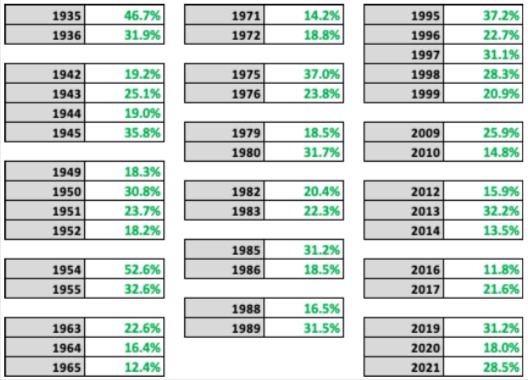

Good Returns Tend to Cluster

It’s human nature to worry about what could go wrong, especially after they have gone really well. Still, it is a mistake to assume that good years in the stock market will be followed by bad years. Consider that momentum is one of the most persistent forces in financial markets. Always remember: “The trend is your friend.” (Until it isn’t!)

Check out this graphic showing how good years tend to cluster together.

As you can see, there is no reason to believe that good years must be followed by bad years.

In reality, the U.S. stock market tends to be positive 2 out of every 3 years. If we think in 10 year intervals, roughly 7 of 10 will be positive and 4 of those years will be highly positive, like between 12% and 30%.

Market Breadth

Our overlords at ChatGPT define market breadth as “the analysis of the number of stocks advancing versus declining in a particular market or index, providing an overview of the market’s overall health and investor sentiment.” In other words, a healthy market would see the majority of stocks rising at the same time.

If you follow the financial news, you tend to hear a lot about the Magnificent 7. It’s the idea that the largest 7 companies in the stock market (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla) accounted for the vast majority of the market’s return in 2023, which is true.

Pundits often point to the dominance of the Magnificent 7 as a reason to be pessimistic about future market returns due to poor market breadth. For example, while the broad stock market was positive thanks to the Magnificent 7, the vast majority of stocks were flat to negative for most of the year.

Since November, however, market breadth has improved dramatically. In fact, market breadth flashed a bullish signal in early December according to this Business Insider articlequotingCarson Group chief marketstrategist Ryan Detrick: “Last week, we saw a very rare breadth thrust, which suggested many stocks were surging, which tends to be a signal of impending strength.”

The article goes on tostate the following:

“Since 1972, this rare signal has flashed 15 times, not counting last week’s signal. The S&P 500 was higher a year later 100% of the time after the signal flashed, generating an average return of 18%.”

Those are pretty good odds.

Outlook &Positioning

We took some profit by trimming back our tech positions at the end of the year. At the same time, we shored up portfolio protection as those strategies had become cheap.

With the exception of investor sentiment, the other indicators we use are in the green. We’ve reached a point where sentiment has become too positive, which indicates lower than average returns in the short-term. Sentiment alone, however, is not reason enough for us to become defensive.

I will start to worry if we see a deterioration in corporate credit conditions. Absent that, the investment environment remains attractive for the time being.

Miscellaneous

Julia is hoping that we get a lot of snow this winter. She’s never lived anywhere that snows, so it’s special to her. Having grown up in the Midwest, let’s just say that I don’t share her enthusiasm.

On a separate note, I hope you all have made resolutions that you can look forward to breaking later in the year. Mine is to lose some weight. We’ll see how long I can make it before gorging myself on a bag of potato chips. Sigh. I think I need to see if our health insurance covers Ozempic.

All kidding aside, I hope everyone has a happy and prosperous 2024! As always, don’t hesitate to reach out to me if you need anything. We’ll talk soon.

Steven Neeley, CFP® is an investment advisor representative of and offers investment advisory services through Fortress Capital Advisors LLC, a registered investment advisor offering advisory services in the State of Indiana and other jurisdictions where registered or exempted.

Sources

The return data for the indexes in the table comes from PortfolioVisualizer.com, an online software platform for portfolio and investment analytics